Believe it or not…

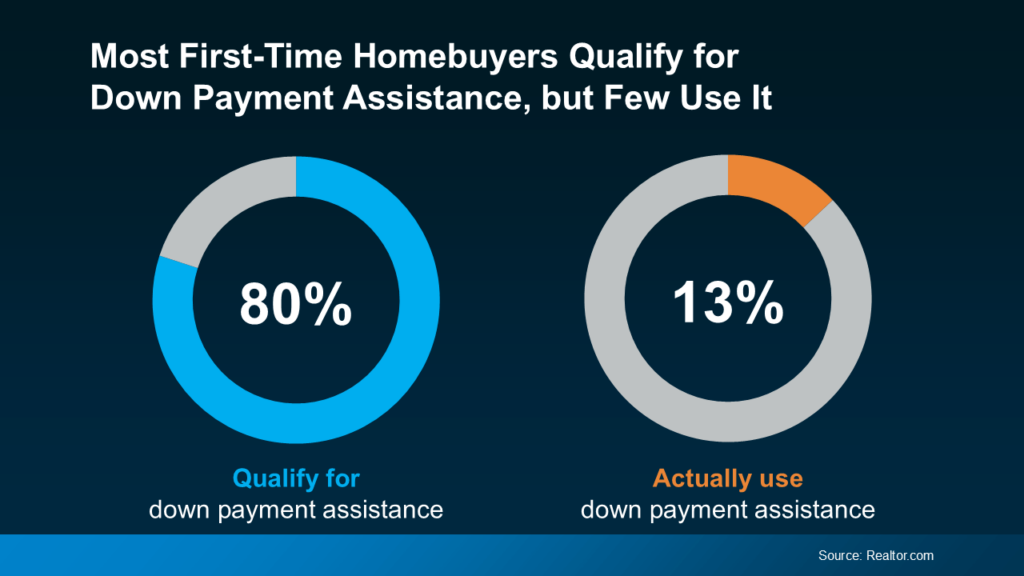

Believe it or not, almost 80% of first-time homebuyers qualify for down payment assistance, but only 13% actually use it. This is a mission-critical gap to close if you are hoping to buy a home.

Here’s what you need to know to make the most of your down payment in today’s housing market.

Amplify Your Down Payment Potential

For the first-time buyers, make sure you’re taking advantage of all the resources designed to help you. Many will get you to your goal faster than you think possible.

There are loan options that require as little as 3% down, or even 0% for certain qualified borrowers, like veterans. There are other payment assistance, like grants that help you cover the upfront cost of your down payment.

If you’re interested in exploring those options, connect with a trusted lender. If you don’t see what’s available, you could be leaving money on the table. You could also be missing your chance at buying a home. These resources can boost your down payment. And a higher down payment could help lower your monthly mortgage payment. It could even avoid or reduce your fees like private mortgage insurance.

Don’t Let News Headlines About Down Payments Scare You

There’s one more thing to address. News coverage has been talking about how the typical down payment is rising. A report from Redfin states:

“The typical down payment for U.S. homebuyers hit a record high of $67,500 in June, up 14.8% from $58,788 a year earlier….This was the 12th consecutive month the median down payment rose year over year.”

But don’t let those high dollars scare you. Just because the average down payment is rising doesn’t mean down payment requirements are going up. That’s a key piece of the puzzle to understand. It’s really because people are choosing to put more down to try to offset higher mortgage rates. Current homeowners who are putting their equity to work are using that to increase their down payment on their next home.

Let’s break those two reasons down a bit:

- A bigger down payment helps lower your monthly mortgage payment. Affordability has been a challenge for many buyers recently. Those who have the ability to make a bigger down payment are going to do so in an effort to lower their future housing costs.

- Buyers who already own a home have a record amount of equity to leverage. Someone who bought a home a few years ago has gained a significant amount of value in their house. These people can put down much more than the average first-time buyer who hasn’t owned a home yet.